Let’s face it — starting a business is no piece of cake. There’s so much that needs to be done. That’s why a business startup checklist is essential to help you keep track of everything.

While your vision and passion are key, success depends on preparation and organization. Without a clear roadmap, even the best business minds can falter.

This comprehensive business startup checklist will guide you through the essential steps, from conducting market research and crafting a business plan to finding capital and running marketing campaigns.

Are you ready to turn your dream startup into a living and breathing business? You’ve come to the right place. Let’s get into it!

A Simple 12-Step Business Startup Checklist

Although different businesses are subject to varying laws depending on their location, some general steps apply to most businesses.

Here’s the business startup checklist to follow when starting your business in the United States.

1. Conduct Market Research

The first thing on your business startup checklist should be market research. The biggest advantage it offers is that it helps you identify your target audience and the potential market size.

Market research highlights consumer behavior and ongoing economic trends to improve your business idea. Knowing your target audience’s demographics and preferences is essential in creating effective marketing campaigns.

Further, market research as part of your business startup checklist minimizes risk by identifying market gaps and potential challenges.

It also helps you identify competitors and understand your product-market fit. Identifying your competitors is especially important as over 4.35 million new business applications were filed last year (2020).

Finally, market research enhances product development. It gives your business insights into what will resonate best with your audience.

For effective results, follow these steps in the checklist.

- Define your purpose: Clarify your business goals in your business startup checklist. Having a clear objective streamlines the research process, making it easier to attain desired results.

- Identify your target market: You can’t target everyone. Adding market research to your business startup checklist helps you segment your audience by age, income, gender, and education level. This lets you design better services and products.

- Choose your research methods: Market research is done in two ways. There’s primary research, where you collect new data from potential customers through surveys. Secondary research, on the other hand, involves analyzing existing data, such as industry reports and statistics. You need both for a better understanding of the market.

- Gather quantitative and qualitative data: Quantitative data is numerical and provides measurable insights like market size, sales figures, or customer demographics. Qualitative data is non-numerical and captures motivations, opinions, and experiences through surveys and interviews. Both give you a well-rounded understanding of the market you’re targeting.

- Test your findings: Before moving on to the next step on your business startup checklist, test your market research findings. Conduct small-scale trials by releasing minimum viable products to gather real-time feedback. Finally, adjust your strategy based on the customer responses you receive.

- Create a report: The last step in this checklist is to compile everything you’ve gathered, including the tests, into an actionable report. Documenting your findings gives you a clear idea of what will work and what will require more time and resources.

Also Read:

- What Are the Benefits of Having Multiple LLCs for Your Business?

- S-Corp Checklist: Essential Steps to Set Up Your Business

2. Design a Business Plan

You also need to create a business plan that talks about how you’re going to carry out your business operations and scale your business. It should also cover your financial plan and projections. This will come in handy when you’re looking for funding.

A well-crafted business plan is a vital part of any business startup checklist and offers several benefits.

First, it helps you secure funding. Banks can’t grant you a business loan and investors can’t fund you if they don’t know what they’re buying into. A business plan provides investors with a clear understanding of your business.

Secondly, a business plan helps you set benchmarks and objectives that keep you focused on your goals. This makes you accountable for your long-term business vision and strategies.

A comprehensive business plan should include the following:

- Executive summary: This is a high-level overview of your entire business plan. It should be engaging and concise, summarizing the business concept, target market, and financial projections.

- Business description: A business description details the industry and market niche your business intends to occupy. It also explains the business structure and the unique value proposition.

- Market analysis: An in-depth analysis of the industry, target audience, and competitors, including market size, trends, customer profiles, and competitive analysis.

- Organization and management: A detailed description of the organizational structure, key team members, their qualifications, and roles. This is where you showcase your consultants and advisory boards.

- Products or services: An explanation of your business offerings, how they meet market needs, and details on production, pricing, patents, and more.

- Operational plan: This section details the key logistics of running the business. It includes location, facilities, technology (such as accounting software), and supply chain management.

- Financial plan: A crucial section for investors that breaks down the financial plan of your business. It includes revenue models, pricing strategies, profit and loss projections, and the use of funds.

- Marketing and sales strategy: This section of your business startup checklist outlines how the business will attract and retain customers. It also covers branding, positioning, sales channels, marketing campaigns, and the projected budget for the entire operation.

Also Read:

- Steps to Starting A Business in Virginia

- How to Register a Business Name in the US: A Guide (Infographic)

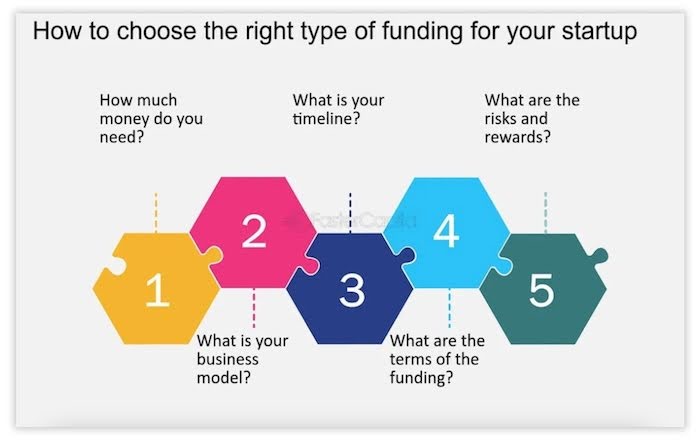

3. Find Business Capital

Sourcing capital involves identifying and securing financial resources to turn your business idea into reality. It’s one of the most critical stages of a business startup checklist.

The first step is figuring out how much funding you’ll need to lay the foundation, considering factors like timeline, risks, business model, and funding terms as shown in the image below.

Image via FasterCapital

Startup costs typically include:

- One-time costs: Business registration fees, leases, deposits, and more.

- Labor costs: Salary for employees or contractors.

- Overhead costs: Office rent, taxes, utilities, product costs, and more.

The next item on your business startup checklist is securing funding. Depending on the scale of your business, you’ll need to explore various options.

Common sources of funding include venture capitalists, angel investors, financial institutions, self-funding, crowdfunding, and government grants.

Each funding source has its own set of rules. Regardless of where you source your funding from, it’s crucial to use funds wisely.

The following mistakes can ruin your business startup checklist. When sourcing funds for your business, avoid these common mistakes:

- Underestimating or overestimating needs: Requesting insufficient funds will leave your business struggling over critical expenses. This can disrupt operations. Borrowing more than you need can also have a negative impact. You’ll have to deal with higher interest rates when repaying.

- Weak business plan: Investors won’t risk investing in a poorly planned venture. You need to craft a detailed business plan strong enough to convince investors and lenders.

- Not reading lending terms: Desperation to secure funding can lead to detrimental agreements. For instance, your lender may demand more control over your business. Read lending agreements before signing anything.

- Ignoring financial advisors: Consulting financial advisors, costly as it may be, will save you from problems. They provide invaluable insight into lending terms and potential risks and advise you on the best path.

- Downplaying regulatory requirements: You’ll need to be compliant with certain legal requirements when seeking capital. For example, equity funding has to adhere to securities laws while crowdfunding must comply with the platform’s terms and conditions. Your business may incur penalties if it bypasses any of these laws.

4. Pick a Strategic Business Location

Choosing the right business location should be a top priority on your business startup checklist. It determines zoning laws, taxes, and other related regulations you’ll be subjected to. Bearing this in mind, the location must be based on strategic decision-making.

There are region-specific expenses to consider, such as startup costs, minimum wage laws, and government fees and licenses. You also need to think about local zoning ordinances, whether you intend to rent or buy business space.

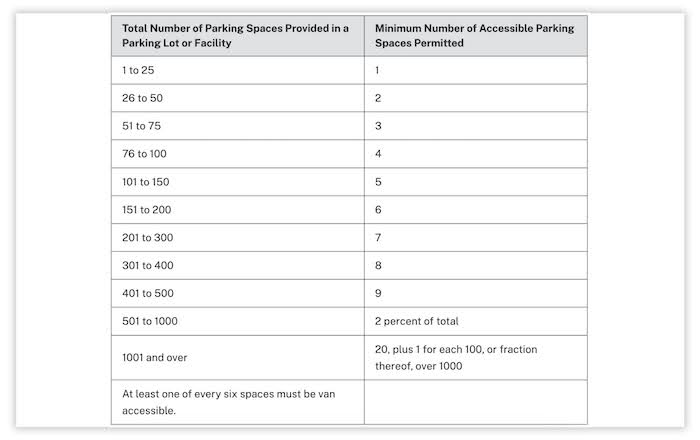

Additionally, your business location must comply with accessibility laws, such as the Americans with Disabilities Act (ADA), which protects people with disabilities from discrimination in public spaces.

Here’s a chart showing the required accessible spaces for parking per ADA guidelines.

Image via Ada.gov

Image via Ada.gov

When choosing prospective locations as part of your business startup checklist, consider the following factors:

- Customer proximity: Set up your business close to your customers for easy access. This is especially important for retail stores and restaurants that require daily patronage.

- Cost implications: Consider rent, utilities, and taxes. All these vary significantly based on the state in which your business is based.

- Competition: Proximity to competitors can be good if you offer better services, but detrimental if they outdo your efforts.

- Workforce availability: A strategic business location should be prioritized in your business startup checklist. Choose a location with access to public transport to attract a wider pool of employees.

- Scalability: Ensure the location can accommodate future expansion. This includes physical space and market reach.

Also Read:

- What Is a Tax ID? Entrepreneur’s Guide to Employer’s Tax ID

- Sole Proprietorship vs S Corp: Pros & Cons Of Each

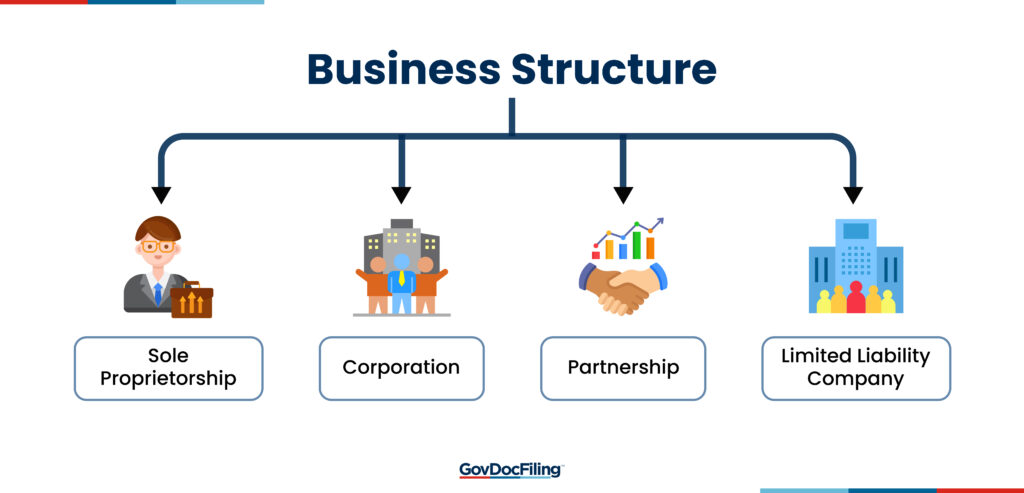

5. Decide on Your Business Structure

A business structure is the legal framework within which a business is organized, making it a crucial item on your business startup checklist. It outlines ownership, profit distribution, taxation, and the roles of everyone involved.

Some common business structures include:

- Sole proprietorship: You have full control, but your business assets and liabilities are tied to your assets and liabilities.

- Partnerships: A legal structure involving two or more people. It can either be a limited partnership (LP) or a limited liability partnership (LLP).

- Limited liability company: An LLC protects you from personal liability, shielding your assets and savings in case of bankruptcy or lawsuits.

- Corporation: A legal business entity that pays corporate taxes, provides liability protection to shareholders, and has a formal management structure.

Deciding on your business structure is important for several reasons.

Your business structure affects how you pay taxes, your liability, and all the paperwork you need to file. For example, a sole proprietorship exposes your assets to risks while an LLC shields against that.

Your business structure also has a huge sway on the ability of your business to attract funding. Venture capitalists, for instance, often prefer corporations with clear ownership structures.

Note that changing your business structure later on can be costly and complicated. You may be subjected to location-based restrictions, unintended dissolution, and high tax penalties, among other complications.

6. Choose a Business Name

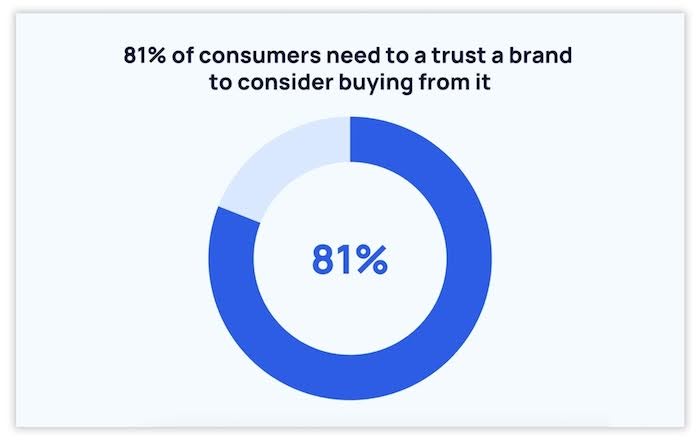

The next thing in this business startup checklist is naming your business. You need to come up with a business name that’s unique, memorable, and easy to spell.

A well-chosen name can make a significant difference, as statistics show that consumers tend to buy from brands they trust. Therefore, it’s important to have a good business name.

Image via Exploding Topics

This would ensure that your audience remembers your business with ease. It must also comply with state regulations.

Additionally, a good business name should reflect your brand identity. It shouldn’t be at odds with the goods and services you’re selling. If you plan to set up an online business, then the name should be easy for search engines to discover.

You need to protect your business name once you settle on the one you like. Registering a business name depends on the business structure and the location. Overall, here are the different types of business names you may need to choose as part of your business startup checklist:

- Entity name: An entity name protects your business at the state level. It’s how the state identifies and interacts with your business as far as regulations are concerned.

- Trademark name: This protects your business name at the national/federal level. The cost of trademark infringement is very high, so ensure you research your name well to avoid issues. Check with your local trademark office if you’re unsure.

- Domain name: A domain name, once registered, protects the website identity of your business. As long as you continue using your registered domain name, no one else can use it.

- DBA name: Doing business as (DBA) is a fictitious name that lets you conduct business under a different identity from your formal business or personal name. It doesn’t provide any legal protection but some states may legally require you to use one for some business structures.

Certain mistakes should be avoided when naming your business or you risk ruining your business startup checklist. Firstly, don’t go with trendy or overused names. They may be catchy right now but they tend to lose relevance over time.

Secondly, choose a name that doesn’t have unintended meanings in other countries if you hope to expand internationally. This includes names that may be derogative in other languages.

Thirdly, don’t skip legal checks to avoid unnecessary legal battles from trademark infringement. Lastly, don’t rush to register a name too quickly. Take your time, test it out so you don’t regret it later. This includes the name you use for the business’s social media accounts.

Also Read:

- What Are the Benefits of Having Multiple LLCs for Your Business?

- Single-Member LLC vs. Multi-Member LLC: How to Choose

7. Register Your Business

Once you’ve selected your business name, the next thing on your business startup checklist is legally registering your business. You could either form an LLC, Sole Proprietorship, Partnership, or Corporation.

Based on the type of business structure you choose, the business registration process will differ. Here’s an illustration of the 6 general steps that may apply to most businesses.

Officially registering a business is important for the following reasons:

- Legal recognition: Registration provides legal recognition for your business, establishing it as a distinct entity. It’s crucial for entering into contracts, securing funding, hiring employees, and operating lawfully.

- Liability protection: Registering some business structures like LLCs protects your assets from business liabilities. This ensures that none of your personal assets are affected when your business is sued or in debt.

- Brand protection: When you register your business you prevent others from stealing or using your brand name. This helps protectyour unique brand identity.

- Access to funding: Proof of registration is necessary when securing funds for your business. A registered business is likely to gain trust and credibility in the marketplace.

In some cases, registering your business name with state and local governments may be sufficient. There are cases where you don’t even need to register at all.

Simply conducting business using your legal name also qualifies as a business registration before the law.

The business structure you adopt determines where and how you register your business. If you’re an LLC, partnership, or corporation, you’ll have to register with the state. This can be done at the office of the Secretary of State, a business agency, or a business bureau.

The cost of registering a business typically ranges from $40 to $300, depending on your business structure and location.

8. Get Your EIN

The next thing to cover in this business startup checklist is getting your Employer Identification Number (EIN). Businesses must get an EIN to hire employees, open a business bank account, and do even the most basic business operations.

Image via Investopedia

You can apply for an EIN in four ways before you start your business. You can do it online, via fax, by mail, or by telephone in the case of international applicants.

Here are reasons why an EIN is an important part of your business startup checklist:

- Tax reporting and compliance: An EIN is necessary for filing taxes, reporting income, and managing business tax obligations. Businesses with employees also require an EIN to submit employee withholding taxes.

- Opening a business account: Financial institutions require an EIN to open a dedicated account. This is necessary for separating personal and business finances as well as protecting you from liabilities.

- Hiring employees: The IRS requires an EIN to track payroll taxes and other necessary contributions like Medicare and Social Security. You also need an EIN to hire employees, which is why it’s an essential part of any business startup checklist.

- Compliance with federal and state laws: Most states require an EIN for registering a business or complying with license and permit agreements. For instance, a business dealing with alcohol, firearms, or tobacco must have an EIN to secure federal permits.

Unlike other legal documents, you can change or replace your EIN if your business structure changes or you relocate your business to another state.

An EIN isn’t mandatory for some business structures like sole proprietorship, unless you plan to hire employees. However, it’s recommended to have it on your business startup checklist to simplify tax reporting.

Also Read:

- Business Legal Name vs. Trade Name: What is the Difference?

- Freelance LLC Guide: Everything You Should Know

9. Apply for Licenses and Permits

Applying for business permits is an important business startup checklist item that you can’t avoid.

You may need to apply for permits and licenses from both federal and state agencies. The fees and specific requirements will vary depending on your location, the nature of your business, and government laws.

For example, licenses and permits for agricultural businesses are different from alcoholic businesses. For alcohol businesses, you need permits from the Alcohol and Tobacco Tax and Trade Bureau and the Local Alcohol Beverage Control Board.

There are ways of knowing which licenses and permits your business needs. Here’s a basic guide for your business startup checklist that you can follow:

- Understand the nature of your business: Define what your business does and know the industry you’re in.

- Check local requirements: Consult with the city or county offices for precise information beforehand.

- Research federal licenses: Investigate to see if your business dabbles in any federally regulated activities like alcohol, then check in with the appropriate agency for guidance.

- Consult experts: Consider getting advice from industry experts with experience in the industry your business is in. Industry-specific organizations can connect you with experienced peers who can offer first-hand advice.

Some of the federal and state licenses and permits you may need to cover in your business startup checklist include the following:

- General business license: This is a license that applies to all businesses, from small freelance business operations to large corporations.

- Zoning permit: A permit that ensures your business location satisfies the local zoning laws. For example, you can’t set up an entertainment club in a zone designated for residential use without approval.

- Health permit: This is essential for businesses handling food services and manufacturing. It ensures compliance with hygiene and workplace safety standards.

- Professional license: This is a permit for professionals like accountants, lawyers, or real estate agents and is usually certified by relevant boards.

- Environmental permits: These are for businesses that impact the environment, such as manufacturing plants that deal with waste disposal or emissions.

Having the right business licenses and permits is good for legal compliance, consumer trust, market access, funding opportunities, and business scalability.

Also Read:

- Essential Legal Documents Every Startup Must Have

- Important Legal Requirements for Starting a Small Business

10. Open a Business Bank Account

For sending and receiving funds, you must open a business bank account. This is essential to ensure that your personal and business finances are separate. It’s also another important thing to include in your business startup checklist.

Start by choosing the right bank with fair fee structures, good business features (such as mobile banking), and easy accessibility. Schedule a meeting on your business startup checklist with a bank representative and address any concerns.

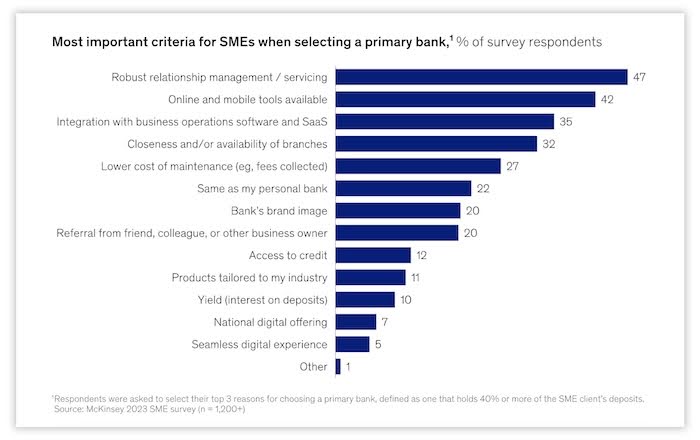

Here’s a 2023 McKinsey survey of what most businesses value most when choosing a bank for their business:

Image via McKinsey

Image via McKinsey

To open a business bank account, you’d typically need to provide the following:

- Government-issued ID documents like passports or driver’s licenses for all authorized signatories.

- Your Employer Identification Number (EIN) for state and federal tax identification.

- Business formation documents (eg., Articles of Incorporation and Articles of Organization) as proof of legal registration.

- Ownership agreements detailing the ownership structure.

- Assumed name certificate (DBA) if your business operates under a different name.

Opening a business bank account has many benefits, which is why it should be on your business startup checklist. Here are some of its key benefits:

- Protection: Separating your personal and business funds offers limited personal liability protection. This means you won’t have to lose personal assets in case the business is sued or forced to file for bankruptcy. A business bank account also offers customers purchase protection by securing their personal information.

- Professionalism: A business bank account enables customers to pay with checks and credit cards to your business instead of doing it directly to you. Further, ticking the business bank account box on your business startup checklist means you can authorize your employees to handle basic banking tasks for the business.

- Preparedness: Having an official business bank account offers you an open line of credit. Financial institutions are more inclined to deal with business accounts than personal accounts. These funds can come in handy for emergencies.

- Building business credit: Having a bank account for your business is a prerequisite for establishing business credit. A good credit history boosts your business’s borrowing potential which enables access to lines of credit and loans for future expansion. So, make sure you add this step to your business startup checklist.

11. Get Business Insurance

Natural disasters, accidents, and lawsuits can jeopardize your business. That’s why getting your business insured should be an important part of your business startup checklist, as it helps protect your business.

Beyond this, the federal government in the United States of America requires every business with employees to get insurance. Businesses with employees are mandated to have workers’ compensation, disability insurance, and unemployment insurance.

Image via Embroker

Image via Embroker

Here are five common types of business insurance you can add to your business startup checklist:

- General liability insurance: It protects your business against financial loss from property damage, bodily injury, libel, medical expenses, settlement bonds, slander, and defending lawsuits or judgments.

- Product liability insurance: It safeguards against financial loss resulting from defective products that may cause bodily harm.

- Professional liability insurance: This coverage protects against financial loss caused by malpractice, negligence, or errors.

- Commercial property insurance: This coverage covers any loss resulting from damage to company property due to wind, fire, hailstorms, vandalism, or civil disobedience.

- Home-based business insurance: This is for home-based businesses and it protects business equipment, office furniture, and third-party coverage.

To ensure you purchase the right insurance, you should add the following steps to your business startup checklist.

- First, assess your risks based on your location. For example, if you’re in hurricane-prone areas, that’s what you’ll want to insure the business against.

- Secondly, work with a reputable licensed agent to find the right policies that match the needs of your business. Thirdly, shop around a little and compare the price and benefits before settling on an insurance option.

- Finally, review and update your insurance every year as your business grows. The more you expand, the bigger your liabilities grow. You need to evaluate the insurance policy to match the changes in your business.

Also Read:

- Best Registered Agent Services for Small Businesses | Govdocfiling

- How to Start an LLC in Florida for Free | GovDocFiling

12. Get the Word Out

The final item on our business startup checklist is marketing.

Effective marketing increases your chances of surviving the first 6 months. Without it, your business may remain obscure, regardless of your efforts.

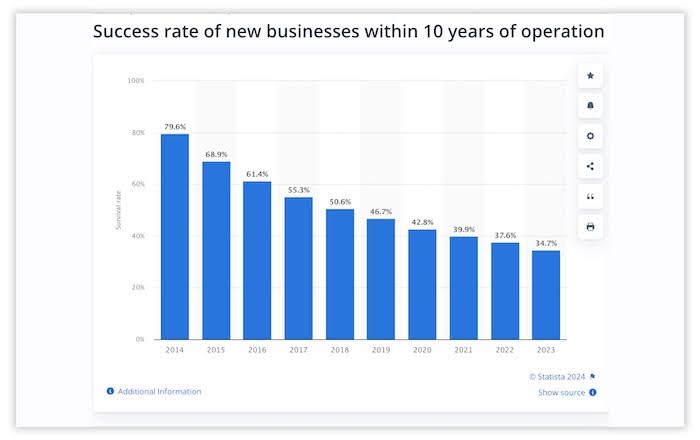

According to Statista, only 34.7% of startups founded between 2013 and 2023 were still operating by mid-2023. This high death rate of businesses is mostly due to a lack of efficient marketing.

Image via Statista

Image via Statista

Marketing should be a priority on your business startup checklist for the following reasons:

- Sets the tone for your brand: Marketing establishes your brand identity, from your logo, tagline, and business name. Maintaining a consistent brand identity builds customer trust and brand recognition.

- Helps you understand your audience: Marketing relies on research which is important in teaching you about who your audience is. It helps you understand their preferences and how they interact with your brand, enabling you to refine your products and services.

- Cost-effective: Marketing is cost-effective when planned early. Scaling marketing campaigns early enables you to test channels, tweak strategies and build a loyal customer base.

- It’s good for funding efforts: Investors and banking institutions need to see evidence of market demand for your products and services before committing their funds. A solid marketing plan shows early traction and this makes your business more appealing to potential investors.

While at it, ensure your marketing is compliant with the advertising laws as stipulated in the Federal Trade Commission Act. Avoid deceptive advertising and familiarize yourself with guidelines on clear disclaimers and truthful claims.

You also have to comply with data privacy regulations like the General Data Protection Regulation (GDPR). These laws require transparency on how customer data is used.

Also Read:

FAQ

1. What should you include in a checklist for starting a business?

You should include your business plan, market research, source of capital, and business location in your business startup checklist. Other important things include business registration, your EIN, licenses, and a sales tax permit.

2. What’s the first essential step before starting a business?

The first essential step before starting a business is creating a business startup checklist that starts with a business plan. This contains an executive summary of the business, market analysis, the products you offer, and marketing and sales strategy.

3. What is the easiest business type to start?

A sole proprietorship is the easiest business type to start. They don’t require too many documents and you’re not usually mandated to separate your personal and business finances. However, it’s highly recommended to separate your finances regardless. This protects you from losing personal assets when the business goes bankrupt or is sued.

4. How do I determine my startup costs?

You can determine your startup costs on your business startup checklist by listing all your expenses. It should include marketing, equipment, legal fees, rent, and any purchase you plan to make, no matter how small it may be. Research the average costs in your industry to create a realistic budget.

5. How do I choose the right structure for my business?

You can choose the right structure for your business when creating your business startup checklist by evaluating your goals, tax implications, and liability concerns. If you don’t want your assets to be affected, then choose an LLC. Other types of structures include sole proprietorship, corporation, and partnership.

Also Read:

Conclusion

If you’re planning on establishing a business, this is what a business startup checklist looks like. Before you even break ground, you’ll have to satisfy a lot of laws, both state and federal. Some tasks, such as conducting market research, and finding business capital are essential.

Others like getting an EIN depend on your business structure but are vital all the same. Go through the business startup checklist when you start your business and ensure you tick as many boxes as possible.